Banks will pay you $300-$400 to open a checking account and route a paycheck through it. Stack three or four of these in 12 months and you can pull in $1,500-2,000 in real cash. The trick isn't finding the bonuses — it's the choreography.

The unsexy financial hack most people leave on the table: banks will pay you to switch checking accounts. Each bank is willing to give you $300-$400 just to open an account and route a paycheck through it for 30-90 days. Stack three or four of these in a 12-month window and you can pull in $1,500-2,000 in real, taxable cash for what amounts to a few hours of bureaucratic work spread across the year.

The trick isn't finding the bonuses. It's the choreography — which one to open first, how to route your direct deposit so it actually qualifies, and when to layer the next one in without tripping anti-fraud flags. Here's the playbook, with the math.

This isn't financial advice. It's a tactical walkthrough of publicly advertised offers as of publication. Promotions change. Your results will vary.

Banks pay sign-up bonuses to acquire customers, because the average banking relationship is worth thousands of dollars in lifetime fees, interchange, and float. From the bank's perspective, paying you $400 once to acquire a sticky depositor is a great deal.

The gatekeeper is the direct deposit requirement. Banks need to verify you're a real working person — defined as someone receiving an ACH from an employer, payroll provider, gig-economy platform, or government benefits payer. The following do NOT count as qualifying direct deposits at most banks:

Bank-to-bank transfers (even if labeled "direct deposit")

Zelle, Venmo, Cash App, or other peer-to-peer payments

Mobile check deposits

One-time deposits like tax refunds

Cash loaded at a retail location

What does count: the same ACH file your employer would send to any bank — coded as payroll, gig income, or government benefits. If you can't route a real paycheck through the new account, you can't unlock the bonus.

Each bank has its own qualifying window (typically 25-90 days from account opening) and minimum amount ($200-$5,000). Bonuses are reported to the IRS on a 1099-INT and taxed as interest income.

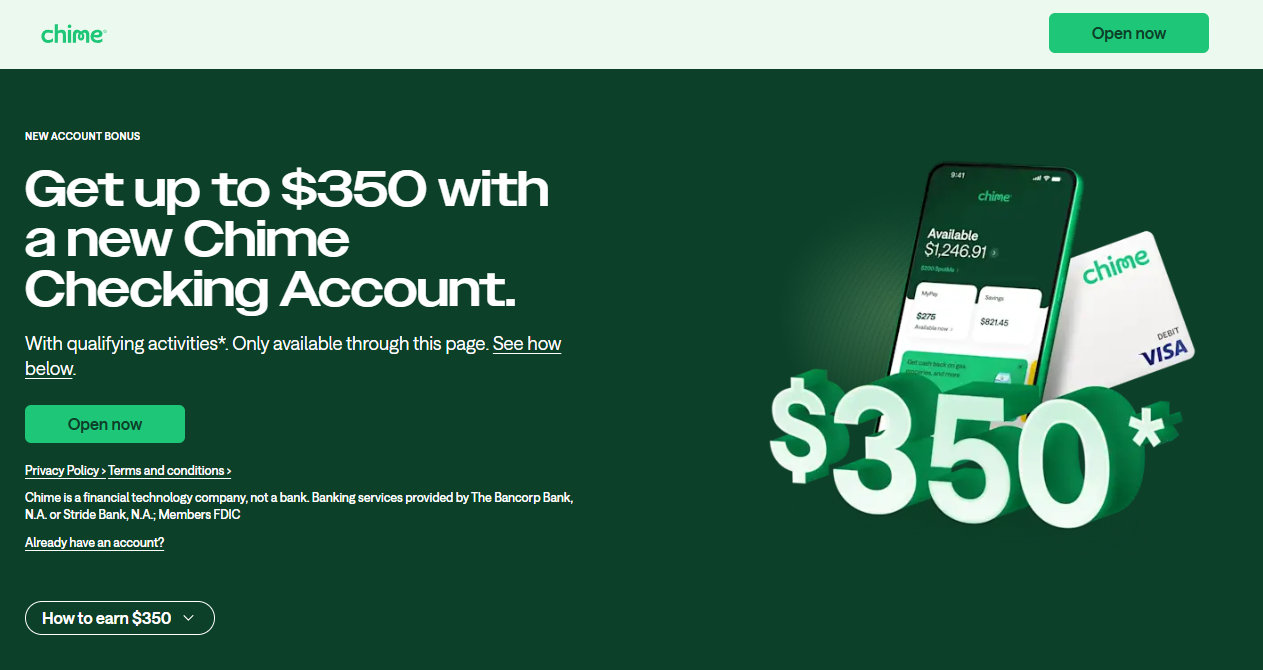

The most accessible bonus on this list because Chime has no minimum balance, no monthly fees, and approves nearly everyone. The bonus structure has two tiers:

$250 for opening your first Chime Checking Account and receiving a qualifying direct deposit of $500+ within 30 days, AND activating your physical Chime Visa card within 14 days of that first deposit.

$350 (the full bonus) requires three consecutive qualifying payroll direct deposits of more than $200 each, with the first arriving within 30 days of signup.

Qualifying direct deposits at Chime are specifically ACH from an employer, payroll provider, benefits payer, or gig payer. Bank transfers, peer-to-peer payments, mobile check deposits, and tax refunds do not qualify — Chime is one of the stricter banks on this point.

Honest take: The full $350 takes about 60 days from signup because you need three consecutive direct deposits to land. If you're paid biweekly, that's two pay cycles. If you're paid weekly, you can be done in about a month. Either way, Chime is the cleanest opener of the stack because there are no monthly fees to worry about if you let the account sit afterward.

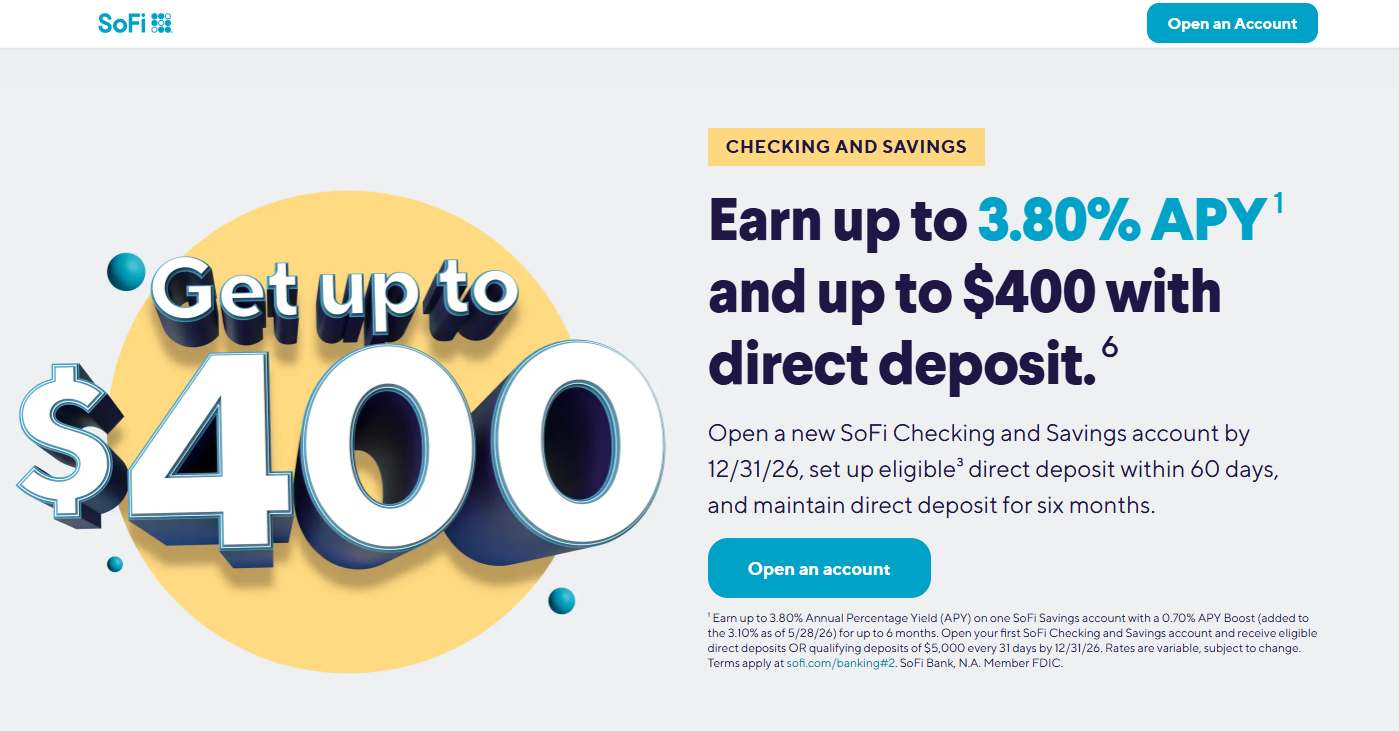

SoFi runs a tiered bonus structure based on how much you direct-deposit in the first 25 days:

$50 with $1,000-$4,999 in direct deposits in 25 days

$300 with $5,000+ in direct deposits in 25 days

For most W-2 earners, the $5K threshold is reachable with two paychecks if you're earning $30/hour+ full time. If your pay is under that, the $50 tier is still worth it for the time invested.

A bonus on top of the bonus: SoFi Checking & Savings currently pays a competitive APY on the savings side (frequently 3.5%+, though it changes with rate cycles). So even after the bonus posts, the money you park there earns more than it would at most big banks.

Honest take: SoFi's qualifying-deposit definition is broader than Chime's — they accept any direct deposit, not just W-2 payroll. If you have gig income, that counts. If you're routing freelance ACH through the account, that counts. Read the latest terms before you assume, but historically SoFi has been one of the easier banks to qualify with.

Open a SoFi Checking & Savings account →

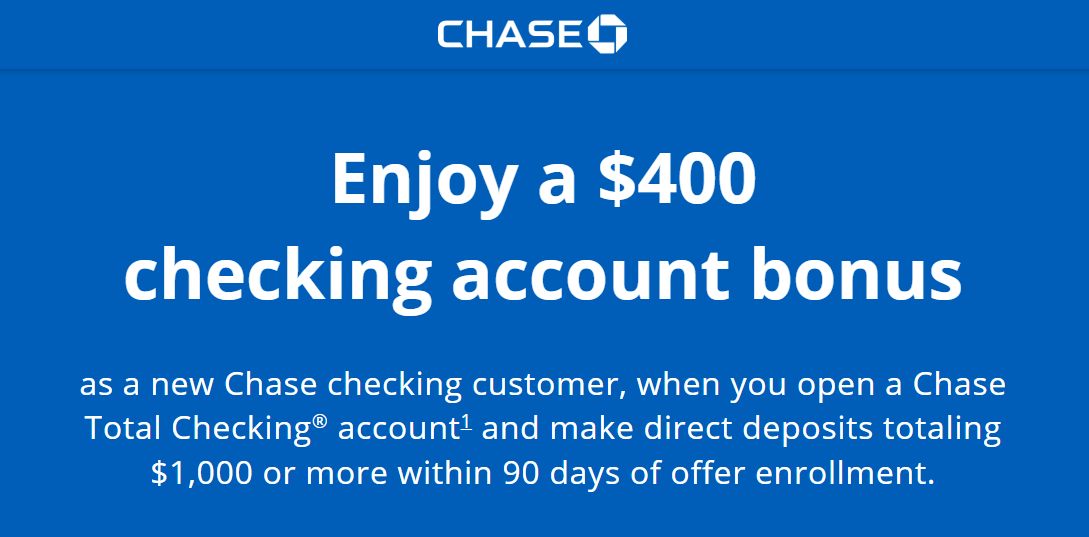

The biggest single bonus on this list, and the lowest direct-deposit threshold to unlock it: $1,000 in cumulative direct deposits within 90 days of opening. Chase's bonus usually posts within about 10 business days of you hitting the threshold.

The catch with Chase: the Total Checking account has a $12 monthly maintenance fee that's only waived if you receive at least $500/month in direct deposits OR maintain a $1,500 minimum balance. If you let direct deposits lapse before the bonus posts AND don't hold $1,500 in the account, you'll start paying $12/mo that quickly eats into your bonus.

Honest take: Chase is the easiest bonus to qualify for and the biggest dollar amount, but it's the one most likely to surprise you with a maintenance fee if you're sloppy. Set a calendar reminder for day 95 — that's after the bonus has posted and you can decide whether to keep flowing direct deposit through or close the account cleanly (after the 6-month minimum hold period — Chase claws back bonuses for accounts closed within 6 months).

Open a Chase Total Checking account →

If you finish Chime, SoFi, and Chase by month 6, you're at roughly $1,050 in pre-tax bonuses. To push past $1,500 in a single year, add a fourth offer for the second half:

BMO Smart Money Checking — $400 with $4,000 in cumulative direct deposits within 90 days

KeyBank Key Smart Checking — $300 with $2,000 in DDs in 90 days (currently using promo code KDMA0526)

Huntington Perks Checking — $400 with $500+ in qualifying direct deposit within 90 days

Discover Cashback Debit — historically $200 bonus, no DD requirement on some promos

Any one of those gets you over $1,500 for the year. Two of them puts you near $2,000.

| Bank | Bonus | Direct deposit needed | Window |

|---|---|---|---|

| Chime | $350 | 3 DDs of $200+ each | ~60 days |

| SoFi (top tier) | $300 | $5,000 in DDs | 25 days |

| Chase Total Checking | $400 | $1,000 in DDs | 90 days |

| BMO Smart Money (optional) | $400 | $4,000 in DDs | 90 days |

| Total (3 banks) | ~$1,050 | ~6 months | |

| Total (4 banks) | ~$1,450 | ~12 months |

After federal tax (22% marginal for most readers), $1,450 in bonuses nets out to roughly $1,130. Still real money for under 10 hours of admin work spread across a year.

Not every fintech account is structured as a sign-up bonus. Two more accounts are worth keeping on the side because they pair well with the bonus chase, even if they don't directly stack:

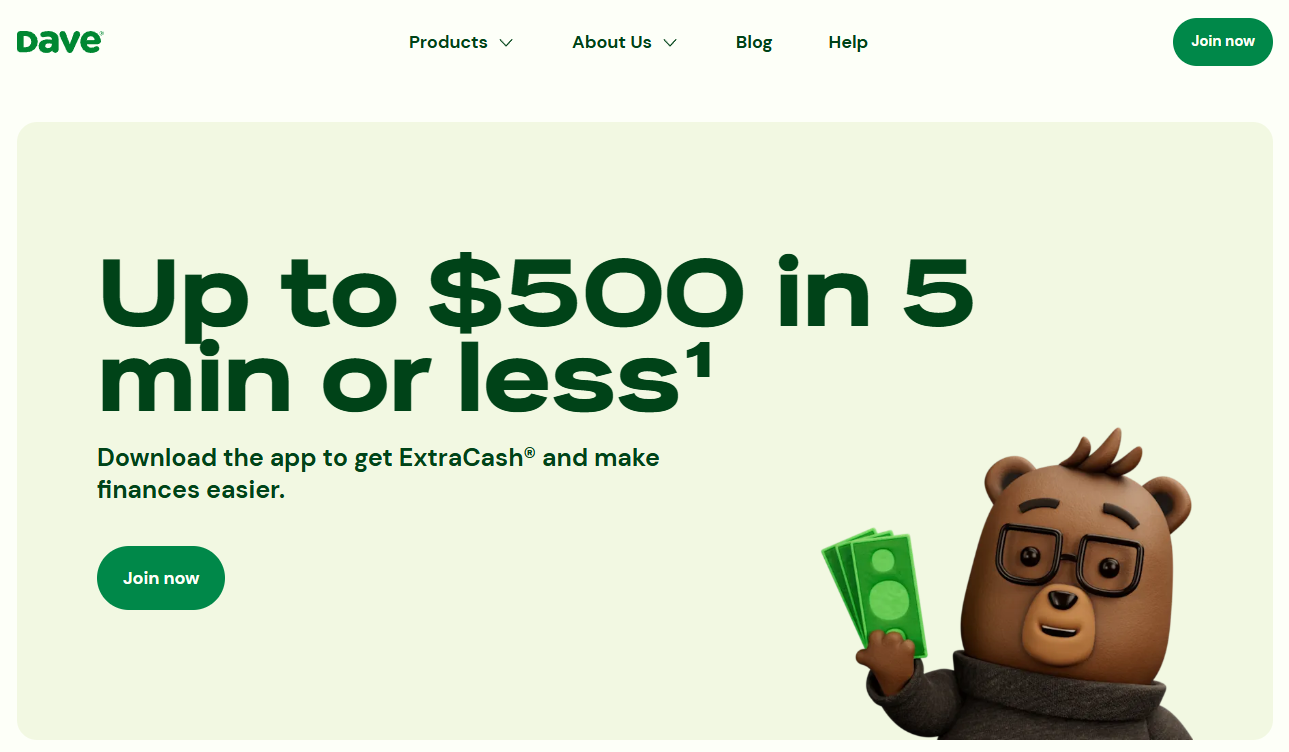

Dave gets you paid up to 2 days early with direct deposit and offers ExtraCash advances up to $500 with no credit check and no overdraft fees. There's a $15 welcome bonus for new accounts.

The reason it pairs well with the bonus chase: when you're routing direct deposits through new accounts to qualify for bonuses, sometimes timing gets tight. Rent is due Wednesday, the new bank's direct deposit doesn't post until Thursday, and you don't want to pay an overdraft fee at your main checking account. Dave's ExtraCash is the bridge for exactly that situation. The $5/mo membership fee is real, but $5 to avoid a $35 overdraft is the cleanest math in personal finance.

Netspend is a prepaid Visa card rather than a true checking account, so it doesn't have a traditional sign-up bonus. What it does have: federal government benefits arriving up to 5 days early with direct deposit, paychecks up to 2 days early, and up to 10% cash back on Netspend Rewards offers at common retailers.

Who this is for: anyone receiving Social Security, SSI, or other federal benefits and wants them earlier. Or anyone who does a lot of everyday shopping at the retailers Netspend Rewards covers — the cash back stacks on top of any credit card rewards you're already earning.

Who this isn't for: a salaried W-2 earner who's just trying to maximize the bank-bonus stack. Stick with the three banks above for that play.

The biggest mistake is opening all four accounts in the same month. Banks pull a ChexSystems report when you open an account, and too many openings in a short window can flag you for fraud review. Space them out:

Month 1-2: Open Chime first. It's the easiest to qualify for, has no monthly fees, and lets you confirm your direct deposit is properly routed through the bonus mechanic before you scale.

Month 3-4: While Chime's last direct deposit is cooking, open SoFi. Adjust your direct deposit splits to route an additional $1,000+ (or $5,000 if you can swing it) through the SoFi account in the first 25 days.

Month 5-6: Open Chase Total Checking. The $1,000 DD threshold is the easiest yet. Once the bonus posts (~day 95), decide whether to keep the account open for the next bonus offer or close it after the 6-month hold.

Month 7-12: Add a fourth bank. BMO is the highest-paying option that requires a lot of DD volume; KeyBank or Huntington are easier qualifiers if your paycheck is smaller.

Qualifying-DD definitions vary. Chime is strict (employer/payroll/gig only). SoFi accepts most direct deposits. Chase falls somewhere in between. Read the current terms — they change.

One bonus per bank, with a holding period. Most banks won't pay a second bonus to the same customer for 12-24 months. The stack only works across different banks.

ChexSystems flags. Banks pull this report when you open. Three openings in 30 days won't usually flag you. Four or five might. Space them out.

Bank bonuses are taxable income. You'll receive a 1099-INT for each bonus over $10. At a 22% federal marginal rate, $1,450 in bonuses becomes a $319 tax bill. Factor that in.

Maintenance fees can erase the bonus. Chase's $12/mo fee, if not waived by ongoing direct deposit, can wipe out the $400 bonus in under three years. Set fee alerts.

Early-closure clawbacks. Most banks claw back the bonus if you close the account within 6 months of opening. Time your closures to fall just after the hold period if you want to free up your direct deposit slot for the next bank.

Routing direct deposit incorrectly. You need the actual ACH file from your employer's payroll system to land at the new bank. A transfer from your old checking account — even one labeled "deposit" — won't count at most banks.

Missing the qualifying window. Each window is 25, 30, 60, or 90 days. Calendar each one as soon as you open the account, with a reminder 5 days before it expires.

Opening all the accounts in the same week. Too many ChexSystems pulls at once looks like fraud-prevention behavior. Space them out by at least 3-4 weeks.

Forgetting to switch direct deposit back. After the third qualifying DD lands at the new bank, switch your direct deposit back to your main account (or split it to the next bonus bank in the queue). Otherwise your main account's bills won't get paid.

Not tracking which DDs counted. If a bonus doesn't post on time, support will ask for specific deposit dates and amounts. Keep a simple spreadsheet — bank, account-open date, qualifying deposits and dates, bonus expected date, bonus posted date.

This week:

Open Chime (the easiest qualifier)

Set up direct deposit through your employer's payroll portal

Calendar day 30 (for the first DD) and day 60 (for the third)

Month 2-3:

Open SoFi while Chime cooks

Route additional direct deposit through SoFi for 25 days

Month 5-6:

Open Chase Total Checking

Set a calendar alert for day 95 to confirm bonus posted

Month 7-12:

Ongoing:

Track all 1099-INTs at tax time

Set fee alerts on accounts with maintenance fees

Don't close accounts until 6 months have passed

The bank-bonus stack isn't glamorous. It isn't a side hustle. It's not even particularly exciting. What it is: $1,500-2,000 in real, taxable cash for the only "skill" being patient, reading the fine print, and keeping a small spreadsheet. The bonuses are publicly advertised. The mechanics are documented. The banks want you to do this — they just want to do it carefully enough that you actually stick around.

If you can route a paycheck through three or four checking accounts in a year, this is one of the highest-hourly-return moves in personal finance. The trick is doing it boringly, in order, without trying to shortcut the qualifying-deposit requirements.

The dollar figures above are based on publicly advertised offers as of publication; promotions change frequently and your results will vary. We may earn a commission when you sign up for offers featured in this article — which doesn't change what we recommend, but you deserve to know.

Join the newsletter your bank hates and your wallet loves.

No spam. Unsubscribe anytime.